4 minutes

Luxury industry faces more selective and reasonable consumers

The global luxury market, which was expected to experience a positive annual growth rate of 3.2% from 2020 to 2022, has seen its trajectory abruptly altered by the coronavirus pandemic.

Today, the most optimistic forecasts predict that the industry will see sales drop by between 35% and 45% in 2020. The experiential luxury segment, including hotels, travel, and cruises, is expected to see an even steeper drop of between 40% to 60%. The Boston Consulting Group released these predictions in a video-conference on consumers and high-end retail, organised by Italian association for luxury goods businesses, Altagamma, on Tuesday.

According to the seventh edition of the ‘True-Luxury Global Consumer Insight’ study, the luxury industry will gradually recover its losses and will not return to how it was in 2019 until 2022 or 2023. This research, carried out by BCG in association with Altagamma, focuses in particular on the tip of the iceberg, meaning the top consumers who spend around €39,000 ($43,960.41) annually on luxury goods.

These customers also found themselves impacted by the Covid-19 crisis and nearly 57% of them said that economic uncertainty has prevented them from making previously planned purchases or investments. For 43% of these luxury consumers, recovery will not take place rapidly. Only Chinese shoppers are more optimistic, as 77% amongst them are betting on a rapid financial recovery.

Customer viewpoints also vary between product categories. For the casual wear and cosmetics sectors, the impact of the virus is expected to be more moderate with a return to normal in two years. However, recovery will take longer for categories including watches, jewellery, and leather goods.

Among the new major market trends, identified by the 12,000 consumers who were interviewed as part of the study, three trends relate to the current period of exiting from the crisis and five are expected to continue in the long-term. As expected, the experiential luxury and tourism industry has been hit hard by the current health crisis, which put an end to cruises and lively nightlife. The top consumers prefer to travel less and stay at home, so they gravitate more towards high-tech products and fine wines with some favouring private and exclusive excursions such as on yachts. Italy, which was once the preferred destination for Chinese and Korean luxury travellers, now comes in third behind France and Japan.

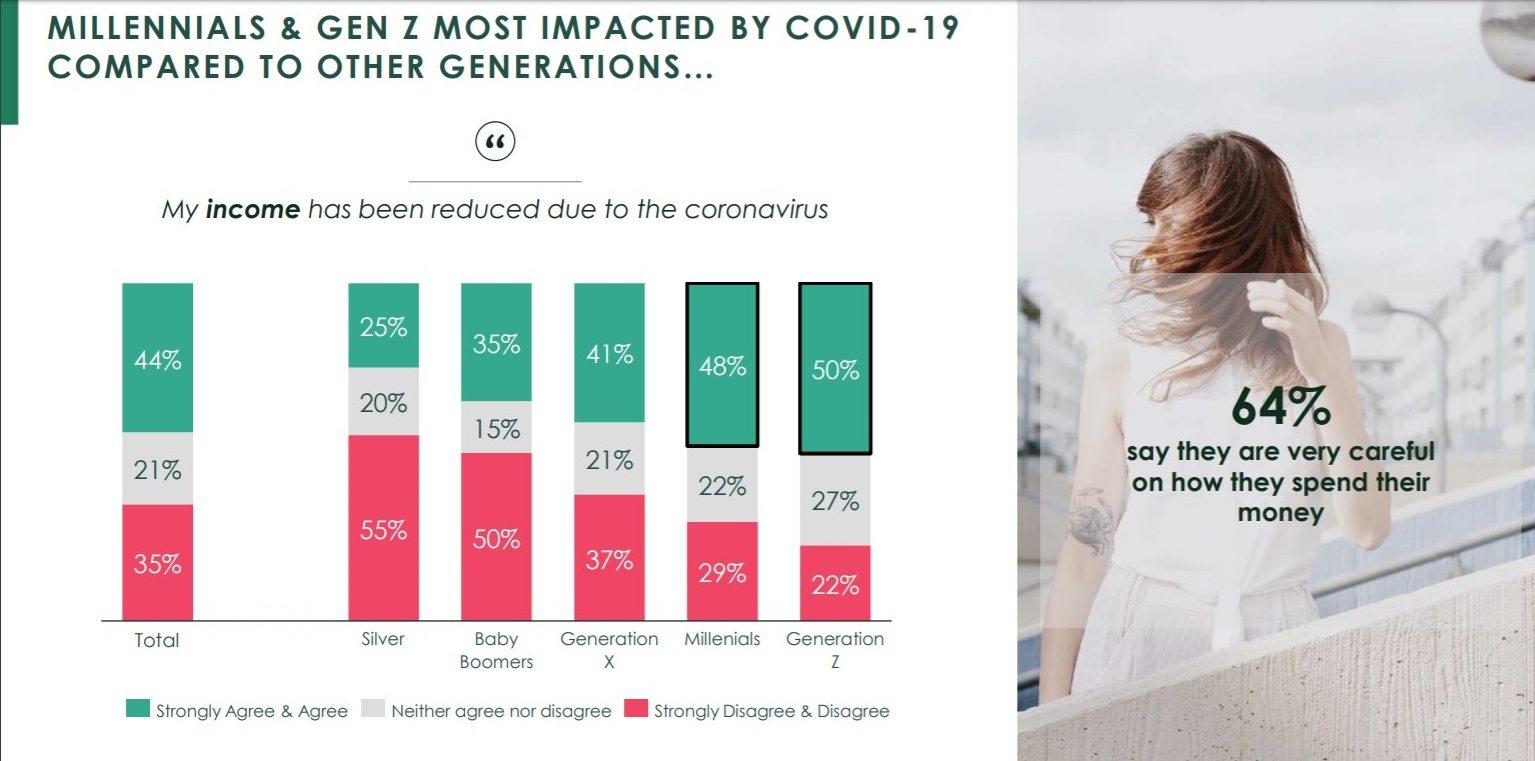

Another effect of the current drop in travel is that Chinese shoppers are consuming more and more in their domestic market, as opposed to around the world. Finally, the third short-term trend concerns a decline in purchases by Millennials and Gen-Z, who have been the most financially affected by the crisis. From now until 2025, these shoppers will represent 55% of total luxury sales. As a result, marketing towards this demographic remains an essential for luxury brands. Almost 60% of the youngest shoppers said that they had been influenced in their decision to make a purchase during lockdown by an advert they had seen on social media, while this was the case for only 25% of older consumers.

Amongst the five trends expected to continue, the authors of the study saw a major polarisation between the West and China. The majority of European and American consumers plan to move towards purchasing from discreet and timeless brands, while Chinese consumers are more attracted to more flashy brands. Whatever strategy luxury brands choose to adopt, the research advocates that it is essential they remain faithful to their brand identity and traditions.

The second long-term trend is the rise of sustainable development within the industry.

“The consumer will henceforth be more selective, favouring 360 degree sustainability,” said Filippo Bianchi, one of the authors of the study.

“Brands will not only have to show production processes that respect the environment, they will also have to adopt a responsible approach in the social sphere and concerning diversity.”

The third trend is the digital personalisation of services offered to customers making online purchases, or ‘Clienteling 2.0’. Used to being pampered in a boutique, ‘true luxury’ consumers expect to be treated just as well in the digital realm. In this context, brands must make a real effort in terms of data, artificial intelligence, and advanced analysis.

The above trend continues into the fourth challenge for luxury businesses, namely, “a new shopping equation balancing online acceleration and in-store experience.”

Following lockdown, more and more consumers are considering buying luxury goods online, to the extent that e-commerce sales are expected to double. Luxury brands must therefore create an online connection, which is perceived as exclusive and which goes beyond what resellers can offer.

Finally, the fifth and final long-term phenomenon that is presenting itself is a boom in the second-hand and rental markets. This activity will eventually be taken over by the brands themselves. Moreover, 70% of people interviewed in the study said that they would like to purchase second-hand products directly from their homes.

In the post-Covid-19 era, more than appearing especially precise, consumers of very high-end products appear, above all, to have become more reasonable.

“In this new reality, they will buy less, more locally, and in a more selective manner,” said the study.

“It is no longer a question of knowing how to sell a certain luxury product, above all it will be about what meaning brands can give to a purchase to turn it from something superfluous into something necessary,” said jewellery brand Pomellato’s CEO Sabina Belli, speaking during the conference.

Copyright © 2024 FashionNetwork.com All rights reserved.